Introduction

ETF VS Mutual Fund . Stock market investing is a critical aspect of wealth accumulation and financial planning for individuals aiming to secure their future. For new investors, understanding the essential principles is an important first step. Fundamental to successful investing is the concept of diversification, which involves spreading investments across various financial instruments to mitigate risk. By diversifying, investors decrease their reliance on a single investment and enhance the potential for stable returns.

There are several investment vehicles available to help diversify a portfolio, and among these, exchange-traded funds (ETFs) and mutual funds have gained considerable popularity. Both options allow investors to gain exposure to a broad range of assets, such as stocks, bonds, and other securities, without needing to select individual investments. This collective investment strategy is especially beneficial for those who are new to investing or who may lack the time and expertise to research individual stocks thoroughly.

Among the benefits of ETFs and mutual funds is their ability to accommodate various investment strategies. For instance, ETFs typically trade on stock exchanges like individual stocks, offering liquidity and flexibility throughout the trading day. In contrast, mutual funds are usually purchased directly from the sponsoring company and are valued at the end of the trading day. Moreover, both ETFs and mutual funds can serve as cost-effective options, as they often have lower fees compared to actively managed accounts.

Ultimately, understanding the nuances of stock market investing, including the significance of ETFs and mutual funds, is crucial for any new investor. By incorporating these investment vehicles into their financial strategy, individuals can work towards achieving their financial goals while maintaining a balanced approach to risk and reward. This comprehensive guide aims to provide insights into the differences between ETFs and mutual funds, enabling investors to make informed decisions that align with their financial objectives.

What is an ETF (Exchange-Traded Fund)?

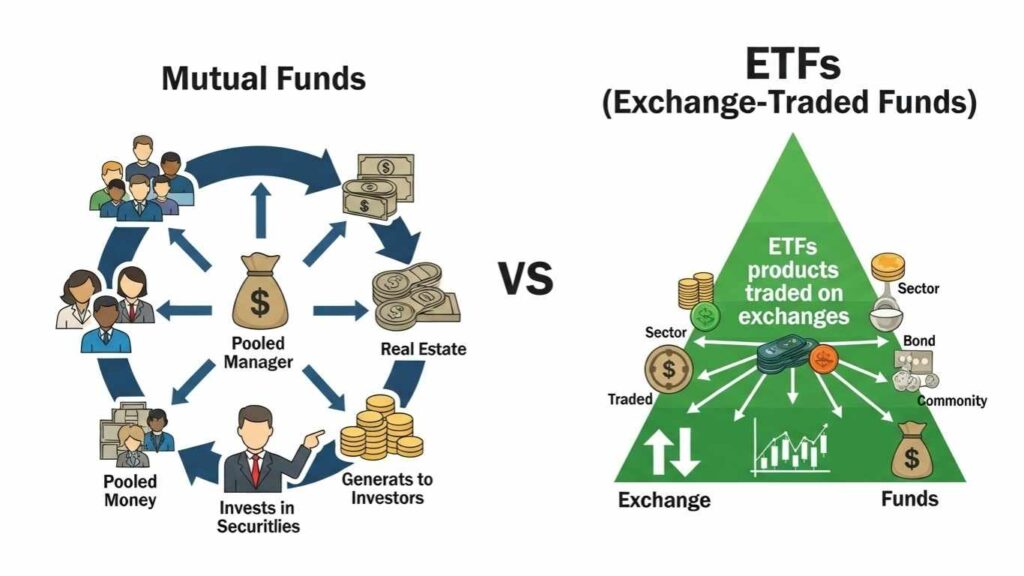

An Exchange-Traded Fund (ETF) is an investment vehicle that combines the characteristics of mutual funds and individual stocks, offering a diversified portfolio of securities to investors. An Exchange traded fund holds a collection of various assets, which can include stocks, bonds, or commodities, allowing investors to gain exposure to a broad market or specific sector without having to purchase each underlying asset individually. The structure of an ETF is designed to provide flexibility and diversification, making it an attractive option for both new and seasoned investors.

Unique to ETFs is their ability to trade on stock exchanges, similar to individual stocks. This structure allows for real-time trading, with prices fluctuating throughout the trading day as opposed to mutual funds, which price at the end of the trading day. Investors can buy and sell Exchange traded fund shares at prevailing market prices, enabling them to react quickly to market changes. Additionally, ETFs can track various indices, providing a cost-effective method to replicate the performance of a specific market benchmark.

One of the primary advantages of ETFs is their generally lower expense ratios compared to mutual funds. This cost efficiency arises from their passive management structure, as many ETFs aim to track indices rather than actively managing a portfolio. Furthermore, ETFs offer tax advantages due to their unique structure, which often results in lower capital gains distributions. This aspect of ETFs enhances their appeal, providing investors with a more tax-efficient way to invest in diversified portfolios.

In summary, ETFs represent a flexible and cost-effective investment option, combining the accessibility of stock trading with the diversification of mutual funds. Their ability to provide continuous pricing, lower expenses, and tax efficiency makes them a popular choice among new investors looking to navigate the complexities of the financial markets.

What is a Mutual Fund?

A mutual fund is a pooled investment vehicle that aggregates capital from multiple investors to invest in a diversified portfolio of assets, such as stocks, bonds, and other securities. Professional fund managers oversee these investments, aiming to achieve specific financial objectives and provide returns to the investors. This collective approach allows individual investors to access a diversified portfolio with relatively lower financial commitment than would typically be required when investing directly in the asset markets.

The structure of mutual funds is characterized by shares that represent ownership in the fund’s overall assets. Investors purchase these shares at the fund’s Net Asset Value (NAV), which is calculated by dividing the total value of the fund’s assets minus its liabilities by the total number of outstanding shares. This NAV is determined at the end of each trading day, providing investors with clarity on the value of their investments. Mutual funds can be bought or sold on any business day, providing liquidity and an entry and exit point for investors.

There are various types of mutual funds available, each catering to different investment goals and risk tolerances. These include equity funds, which invest primarily in stocks; bond funds, focusing on fixed income securities; and balanced funds, which combine both stocks and bonds. Additionally, money market funds invest in short-term, low-risk instruments, making them suitable for conservative investors. Each type of fund offers distinct advantages, such as exposure to certain market segments or a specific investment strategy.

One of the key advantages of mutual funds lies in their professional management. Investors benefit from the expertise and insights of fund managers, who conduct extensive research to inform their investment decisions. Moreover, mutual funds typically offer automated diversification, reducing investment risk by spreading capital across a variety of assets, which is particularly valuable for new investors seeking to build a comprehensive investment portfolio.

Key Differences Between ETFs and Mutual Funds

Exchange-Traded Funds (ETFs) and mutual funds serve as popular investment vehicles, but they exhibit several critical differences that influence investors’ choices and strategies. One of the primary distinctions lies in their trading mechanisms. ETFs are traded on an exchange like individual stocks, allowing investors to purchase and sell shares throughout the trading day at market prices. This mechanism provides a significant advantage in terms of liquidity, enabling quick transactions that can be executed instantly, an essential factor for many traders. In contrast, mutual funds are bought and sold at the end of the trading day, with all transactions executed at the day’s closing price, potentially limiting the ability to respond to market fluctuations swiftly.

Another notable difference is their fee structures. Generally, ETFs have lower expense ratios compared to mutual funds, primarily because they are passively managed and do not require the same level of active management. This cost efficiency can lead to more significant long-term returns for investors. However, investors must also consider trading costs associated with ETFs, which may include brokerage fees. Mutual funds may have no transaction fees but could impose redemption fees or loads, which can increase overall costs depending on the investment approach.

Tax implications vary significantly between the two investment types as well. ETFs typically enjoy greater tax efficiency due to their unique structure, which allows investors to buy and sell shares without triggering capital gains taxes. On the other hand, mutual funds may distribute capital gains to shareholders at the end of the year, potentially resulting in unexpected tax liabilities. These differences necessitate careful consideration regarding investment strategies, as they can impact portfolio performance over time. Hence, understanding how these distinct factors align with individual investor profiles is key in determining which investment vehicle is most suitable.

Cost Considerations: Fees and Expenses

When evaluating investment options like ETFs (Exchange-Traded Funds) and mutual funds, understanding the costs associated with these vehicles is crucial for maximizing returns. Both ETFs and mutual funds come with various fees, and investors need to be aware of these costs to make informed decisions.

The primary cost linked to both investment types is the expense ratio, which represents the annual fees expressed as a percentage of the fund’s average net assets. Expense ratios can significantly impact long-term returns, as even small differences can compound over time. Typically, ETFs have lower expense ratios compared to mutual funds, making them an attractive option for cost-conscious investors.

Another critical component of the cost structure is management fees, which compensate fund managers for their investment expertise. While actively managed mutual funds often have higher management fees due to the hands-on approach of the fund managers, passively managed ETFs generally have lower fees. This difference is particularly noteworthy for investors looking to minimize fees and maximize returns.

In addition to these fees, commission costs can also affect profitability, especially for ETFs, which trade like stocks on exchanges. Most brokerage firms charge a commission for buying and selling ETF shares, although many have recently eliminated trading fees for certain funds. Conversely, mutual funds may come with sales loads, which are one-time charges applied at the time of investment or redemption. Understanding these costs is vital for identifying the more cost-effective option.

Finally, hidden fees can lurk in both investment vehicles, including transaction fees or performance fees in mutual funds. Therefore, investors must scrutinize the fund prospectus and other provided documentation to uncover any potential hidden charges. By conducting this thorough assessment of fees and expenses, investors can choose the most suitable option based on their individual financial situations and investment objectives.

Risk Tolerance and Investment Goals

When considering investments, understanding one’s risk tolerance and investment goals is crucial, particularly in the context of choosing between exchange-traded funds (ETFs) and mutual funds. Risk tolerance refers to an investor’s capacity and willingness to endure fluctuations in the value of their investments, while investment goals relate to what an investor hopes to achieve, be it capital preservation, income generation, or capital appreciation. These foundational aspects significantly influence the appropriate investment vehicle.

Investors can generally be classified into three risk profiles: conservative, moderate, and aggressive. Conservative investors typically seek stability and prioritize capital preservation, often gravitating towards low-volatility investments. Mutual funds, particularly those focused on bonds or stable blue-chip stocks, might be more attractive to this group due to their managerial oversight and traditional structure. In contrast, aggressive investors may favor ETFs, harnessing their potential for higher returns through exposure to a broader range of assets, including volatile stocks or commodities.

It’s also vital to factor in the investor’s time horizon. Short-term investors, who anticipate needing access to their funds within a few years, might prefer mutual funds for their structured management and the potential for less price fluctuation. Conversely, long-term investors can tolerate short-term volatility and may lean towards ETFs, which often come with lower expense ratios and tax efficiency, particularly in capital gains realization, making them suitable for a buy-and-hold strategy.

Ultimately, aligning one’s risk profile and investment horizon with the characteristics of ETFs and mutual funds plays a pivotal role in making an informed decision. This alignment ensures that the chosen investment vehicle effectively addresses both current financial circumstances and future aspirations.

Tax Implications of ETFs and Mutual Funds

When evaluating investment options, understanding the tax implications of exchange-traded funds (ETFs) and mutual funds is crucial for a new investor. Both of these investment vehicles offer distinct characteristics that influence their tax treatment. A key difference lies in how capital gains are incurred and reported for each type of fund.

Mutual funds tend to distribute capital gains to shareholders at the end of the year, reflecting the profits generated by the underlying securities sold within the fund’s portfolio. These capital gains distributions are typically subject to taxation in the year they occur, even if investors do not sell any shares themselves. Consequently, investors could be liable for taxes on gains generated by assets that they did not personally sell, potentially resulting in an unexpected tax burden.

On the other hand, ETFs are generally regarded as more tax-efficient due to their unique structure. When investors buy or sell shares of an ETF, they are transacting on an exchange, which allows for the creation and redemption of shares without directly selling the underlying securities. This mechanism minimizes the occurrence of realized capital gains within the fund itself, leading to fewer taxable events for shareholders. Consequently, ETF investors might have more control over their tax situations, allowing them to defer taxes until they decide to sell their shares.

Another factor to consider is the type of account in which these investment vehicles reside. Holding ETFs or mutual funds in tax-advantaged accounts like IRAs or 401(k)s can offset some of the tax implications since taxes can be deferred until distributions are taken. However, understanding the underlying tax treatment of each investment type is essential for effective tax management and planning.

In conclusion, new investors should carefully consider the tax implications of ETFs and mutual funds, as these factors can significantly influence their overall investment strategy and tax efficiency.

Practical Steps to Get Started

For new investors looking to venture into the world of individual securities, Exchange-Traded Funds (ETFs) and mutual funds present an accessible gateway. To get started, it is crucial first to evaluate fund performance. This involves researching historical returns, risk metrics, and expense ratios of various funds. Tools like Morningstar or fund provider websites can offer valuable insights into these characteristics. Focusing on funds with a consistent performance track record and reasonable fees can lead to better long-term results.

Once you have identified potential funds, the next step is to open an investment account. Most brokerages offer platforms specifically designed for new investors, providing user-friendly interfaces and resources for guidance. Decide whether to choose an online broker, a robo-advisor, or a traditional financial advisor based on your preference for control versus convenience. Ensure to confirm that the brokerage offers both ETFs and mutual funds to give you flexibility in your investment choices.

Building a diversified portfolio is essential in mitigating risks while pursuing growth. This can be achieved by investing in a mix of asset classes, such as stocks, bonds, and real estate, through both ETFs and mutual funds. Diversification can help cushion the impact of volatility in specific sectors or regions. As a rule of thumb, consider allocating a percentage of your portfolio to different asset classes based on your risk tolerance and investment horizon.

Finally, continuously monitoring your investments is vital to ensure they align with your changing goals and prevailing market conditions. Periodically review your portfolio’s performance and adjust your asset allocations as necessary, taking into account factors such as market trends and personal financial objectives. Being proactive can lead to more informed decisions and lasting investment success.

Conclusion: Making the Right Choice for You

In navigating the investment landscape, it’s imperative to understand the distinctive characteristics of both Exchange-Traded Funds (ETFs) and mutual funds. Each investment vehicle offers unique advantages and disadvantages that can significantly influence your financial outcomes. Therefore, the decision to invest in ETFs or mutual funds should be aligned with your individual financial goals and risk tolerance.

ETFs typically provide lower expense ratios, greater flexibility in trading, and tax efficiency, which can be attractive features for many investors. On the other hand, mutual funds might be more suitable for investors seeking professional management and the convenience of automatic investment plans. Understanding these features and how they align with your investment strategy is crucial. It’s important to assess whether the potential for cost savings with ETFs outweighs the benefits of the hands-on management offered by mutual funds.

Moreover, consider your investment timeline, liquidity requirements, and how involved you wish to be in managing your investments. New investors are often encouraged to take a cautious approach, gradually expanding their knowledge base as they prepare to make informed choices. Engaging with educational resources or consulting with a financial advisor can provide the necessary insights to navigate these decisions effectively.

Ultimately, the best choice between ETFs and mutual funds will vary based on personal circumstances and preferences. By carefully analyzing the features and costs associated with each option, you can make a more informed decision that supports your financial objectives. Remember that external factors, such as market conditions and your evolving financial situation, may also play a role in your investment strategy over time.